By Spy Uganda

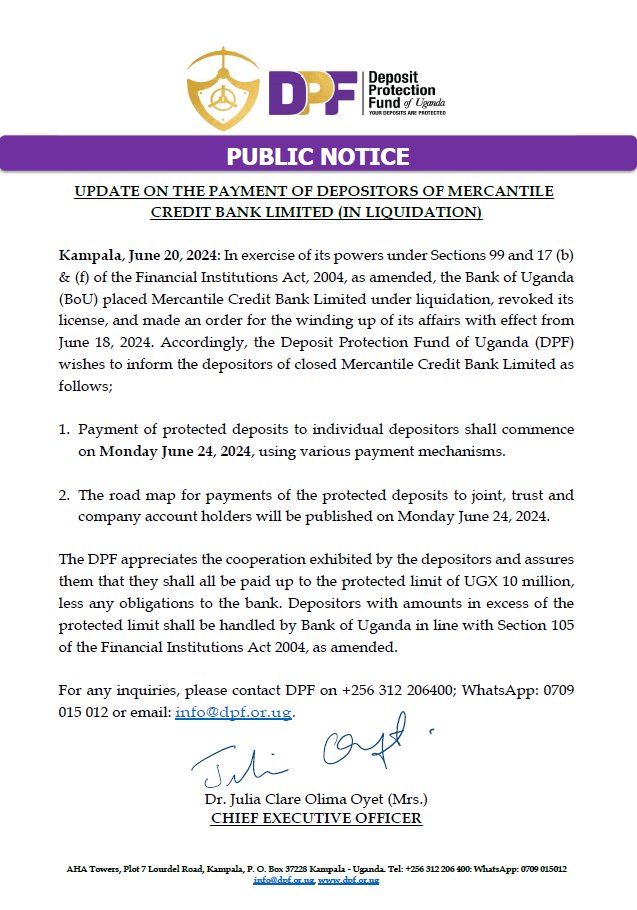

Kampala: In the past six months, Ugandans have been shocked with the closure of two key banks, EFC Uganda Limited (MDI) closed on 19 th January 2024 and most recently Mercantile Credit Bank Limited (MCBL), on 18 June 2024.

The reasons put forward by the Bank of Uganda (BoU) for Closure among others have been Under capitalization and insolvency. Liquidation processes by the Central bank have turned into a very painful story for Ugandan investors and business community.

First, the Deposit Protection Fund (DPF) Insurance of 10M Shillings of total customer deposits is not practical to doing business and banking in Uganda , This threshold must be revised upwards otherwise there is no confidence in the safety of business deposits, One wonders with all the over 500 MPs, why such a problem has not been raised yet the DPF stickers and placards on the insured amount of 10M Shillings are displayed in all banking halls.

In all these closures of banks, a notice in the public newspapers quotes section 105 of the financial institutions act 2004 as amended which talks of order of payments for the un insured amount above shs10m (Payment of creditors and ranking of claims).

Section 105- Payment to Creditors and Ranking of Claims

(1) The liquidator shall, within two months after submission of a report of the assets and liabilities of the financial institution commence the payment to depositors and creditors of the financial institution except that—

(a) payment shall be made first to the Deposit Protection Fund;

(b) second to the liquidator for all expenses incurred in the process of liquidating the financial institution;

(c) third to employees for all wages and salaries due net of any liabilities to the financial institution;

(d) fourth to secured creditors in pari passu;

(e) fifth to depositors for deposits which are in excess of the protected deposit amount;

(f) then to other creditors to rank in pari passu.

(2) Section 315 of the Companies Act shall not apply to a liquidation of a financial institution.

(3) Where any assets remain after the payment by the liquidator of all claims against the financial institution, the remaining assets shall be distributed among the shareholders in accordance with their respective rights and interests.

The fundamental questions that arise is Central Bank has played the role of the liquidator in all these cases , why do they then charge fees , and the law allows them to determine their own fees as seen in (b) above , This money they are paying themselves belongs to the business community (Depositors) If this is not corruption and a bad law , one wonders why a government led by a Renowned freedom fighter H.E Excellency Rtd (but not tired) General Yoweri Kaguta Rutahaburwa Museveni Ruhembagwenjura would keep such exploitative laws.

Also for businesses, Investors and depositors beyond the shs10m mark are subjected to the delays of many years before getting back their funds which are the blood stream of their businesses. This has led to business collapse and unfortunately the Central Bank and the government are completely blind on the matter. Their feasibility studies of closure are always poor and the colonial exploiters at the central bank are always waiting for another liquidation to play around with unsecured monies of depositors. Unfortunately the government loses tax payers, many are left unemployed after closure of these companies, As a matter of fact several companies will always collapse with banks closures. What has parliament done to protect the business community. What can be done differently in this process to ensure that Ugandan businesses are not harmed?

We also wonder if in absence of a governor of Central Bank, if such closures are legal, does the law allow an acting or deputy governor to institute such action? By the way, in the entire history of mankind, did you know that Michael Atingi-Ego is the first human being to deputize a dead body for 4 yrs? I mean, if you’re a deputy to some one, it means you have a boss you report to. Question; which taxis does Atingi-Ego board to take reports to his boss? when does he seek advice from his boss?! I’m talking about 4 yrs of deputizing a ghost and it’s business as usual at BoU!

How will the business community have the confidence to keep their money in the bank if your insured amount is so low, and the central bank is very okay with this, This will explain why currently out of 10 Ugandan businessmen 6 keep their money at home and in their houses. Is this the beginning of collapse of the banking sector?

Research done on these closures reveal that final liquidation reports take several years to be tabled , the business community continue to bear this un-certainity and this continues to cripple businesses.

Central bank needs a non-corruptible and clear headed tested leader to give confidence to the business community.

We are aware of past Bank of Uganda scandals surrounding liquidation (Justine Bagyenda BoU Scandal) and we believe that such a very sensitive exercise should not be left to the usual vultures at the central bank but closely monitored by the Investor Protection Unit of State House led by the no nonsense Col Edith Nakalema.

We hope that our many legislators can pick up such matters that continue to discomfort the business community and also revise the Insolvency Act which is not only out of touch with the business practices in Uganda but another colonial exploitative law.